Effective risk management for small business is all about identifying, assessing, and controlling threats to your company’s bottom line. Think of it less as avoiding all danger and more as building a resilient operation that can see challenges coming, protect its assets, and confidently grab opportunities when they appear.

Why Risk Management Is Your Business Superpower

Let's be real—running a small business can feel like trying to steer a ship through a sudden squall. You can't control the weather, but you can build a sturdier ship, train your crew, and carry a reliable map. That map is your risk management plan. It’s not just some defensive chore; it’s a powerful tool that gives you a serious edge.

Instead of just reacting to problems after the damage is done, a proactive approach helps you look ahead. It turns that knot of uncertainty in your stomach into a manageable part of your business strategy. Once you understand the potential pitfalls, you can start making smarter, bolder decisions.

Build a More Resilient Foundation

A solid risk management framework does more than just stop you from losing money. It helps you build a durable business that can weather economic downturns, supply chain hiccups, or unexpected market shifts. This kind of resilience is crucial, especially when you consider how much small businesses contribute.

In the United States, about 95% of businesses are considered small. They’re the backbone of the economy, generating nearly half of all sales and creating roughly 60% of new jobs. With so much riding on their success, having a plan to navigate uncertainty is vital for both survival and growth. You can dive deeper into their economic impact in this detailed entrepreneurial overview.

Gain a Competitive Edge

A lot of your competitors are probably stuck in a reactive mindset, just putting out fires as they pop up. When you proactively manage risk, you set your business up to be more stable, reliable, and trustworthy in the eyes of customers, partners, and even lenders.

This strategic foresight pays off in a few key ways:

- Enhanced Reputation: A business that handles challenges without skipping a beat builds confidence and a strong public image.

- Improved Decision-Making: With a clear view of potential threats, you can put your resources where they matter most and chase growth opportunities with more confidence.

- Financial Stability: Protecting your assets and cutting down on surprise costs directly strengthens your bottom line and sets you up for long-term profitability.

At the end of the day, risk management for small business isn’t about creating a mountain of paperwork. It’s about building a culture of awareness that empowers you to protect what you’ve built and steer your company toward a more secure, prosperous future.

How to Spot Dangers Before They Strike

Before you can manage risk, you have to find it. But here’s the thing: most major threats don’t show up with a flashing neon sign. They creep in quietly, often hidden in the hustle of your daily operations. That's why the first real step in risk management for small business is learning how to spot these hidden dangers before they turn into bigger problems.

Think of yourself as a detective for your own company. Your job is to constantly look for clues—the little cracks in the foundation that could widen over time. This isn’t a one-and-done task; it’s about building a habit of awareness. By actively looking for what could go wrong, you shift from being a reactive owner constantly putting out fires to a proactive leader who sees them coming and steers clear.

To make this easier to tackle, we can break down potential threats into four distinct categories. This helps organize your thinking so you're not overlooking a critical part of your business.

Four Core Areas of Business Risk

Just about every problem your business might run into falls into one of these four buckets. Thinking about them this way keeps the process from feeling overwhelming and gives you a simple framework for your detective work. You can even use these categories as a checklist to methodically scan your operations.

The four main types of risk are:

- Financial Risks: These are dangers tied to the money flowing in and out of your business. For most owners, this is top-of-mind.

- Operational Risks: These threats pop up from your internal processes, systems, and people—the moving parts that keep your business running each day.

- Strategic Risks: These are the bigger-picture, external risks linked to your spot in the market and the long-term decisions you make.

- Compliance Risks: These risks come from the web of laws, regulations, and industry standards you’re expected to follow.

To get your gears turning, the table below breaks down these categories with some practical, real-world examples. Use it to start thinking about where your own business might be vulnerable.

Common Risk Categories for Small Businesses

This table breaks down common risk types with practical examples to help you identify potential threats in your own operations.

| Risk Category | Description | Example Scenarios |

|---|---|---|

| Financial | Threats to your company's cash flow, profitability, and overall financial health. | A major client paying their invoices 60 days late, a sudden increase in material costs, or a credit line being unexpectedly reduced. |

| Operational | Dangers stemming from failures in your day-to-day processes, systems, or people. | A key piece of equipment breaking down, a critical supplier going out of business, or the loss of a key employee with unique knowledge. |

| Strategic | External threats related to your market, competitors, and overall business strategy. | A new competitor opening across the street, a major shift in consumer tastes, or a negative review going viral online. |

| Compliance | Risks of failing to adhere to legal, regulatory, or industry standards. | Mishandling customer data in violation of privacy laws, failing to meet workplace safety standards, or using unlicensed software. |

Once you’re familiar with these areas, you can start digging in to find specific risks. You don't need a team of expensive consultants to do it, either.

Simple Methods for Uncovering Risks

Identifying risks doesn’t require fancy software or a big budget. You can get started today with a few straightforward techniques that tap into the knowledge you and your team already have. The goal is to create a master list of potential challenges.

A team brainstorm is one of the most powerful places to start. Your employees on the front lines see things you don’t. Ask them directly: "What keeps you up at night about your job? What could go wrong that would stop us from serving our customers?"

By asking "What could go wrong?" and "How would it affect the business?", you begin to map out potential problems. This simple questioning process is the foundation of building a resilient business prepared for surprises.

Another fantastic tool is a quick SWOT analysis (Strengths, Weaknesses, Opportunities, Threats). The "Threats" section is tailor-made for risk identification, pushing you to think about external factors like market trends and competitors. Finally, don't forget to look backward. Review past mistakes. Did a project go off the rails? Did you lose a key client? Analyzing what went wrong is a goldmine of insight for preventing it from happening again.

A Simple Four-Step Framework for Managing Risk

So, you’ve brainstormed a list of potential threats. What now? The sheer number of possibilities can feel paralyzing, making you want to just shove the list in a drawer and hope for the best.

But effective risk management for small business doesn't need to be a bureaucratic nightmare. It’s really just a logical process you can follow over and over.

Think of it like spring cleaning your business. You wouldn't just start randomly throwing things out. First, you’d figure out what’s junk and what’s valuable. Then, you’d decide whether to toss it, store it, or fix it up. Finally, you'd make a plan to keep things tidy so the mess doesn't pile up again. Risk management follows that exact same logic, broken down into a simple, four-step cycle.

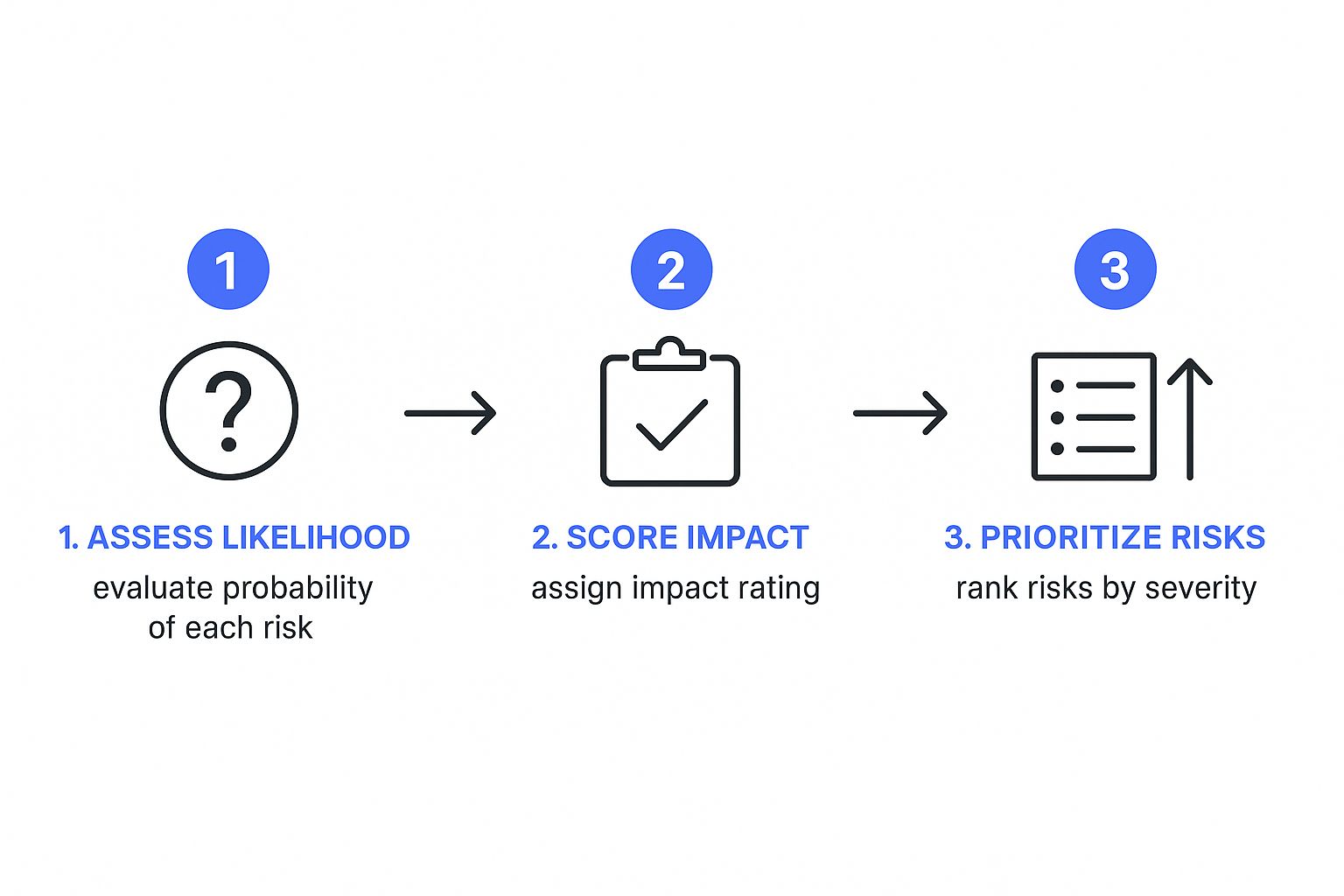

Step 1: Assess the Risk

Let’s be honest: not all risks are created equal. The chance of your office flooding is a completely different beast than the chance of a key employee quitting. The first step is to look at each risk you’ve identified and figure out how bad it could really be. This is all about prioritizing so you can focus your energy on the threats that actually matter.

To do this, you’ll want to evaluate each risk using two simple factors:

- Likelihood: How probable is it that this event will actually happen? A simple Low, Medium, or High scale works perfectly.

- Impact: If it does happen, how much damage would it do to your business? Again, stick with a Low, Medium, or High scale.

A risk with a high likelihood and a high impact (like a critical piece of equipment failing) rockets to the top of your list. A risk with low likelihood and low impact (like a minor supplier being a day late with a delivery) can wait.

This chart breaks down the basic flow for sizing up and ranking your risks.

As you can see, assessment isn't just one action. It's a sequence: evaluate the probability, score the potential damage, and then use that data to rank what needs your attention most urgently.

Step 2: Mitigate the Threat

Once your risks are assessed and prioritized, it's time to decide what to do about them. This is the "action" part of the plan. For any given risk, you have four possible responses. Your choice will come down to the risk's severity and what your company can realistically handle.

The core of risk mitigation is making a conscious choice. Instead of letting circumstances dictate your future, you decide how to confront each potential threat, giving you back control over your business's destiny.

Here are your four main strategies:

- Avoid It: Sometimes the best move is to change your process to eliminate the risk entirely. If a specific service is a consistent money-loser and a source of customer complaints, you might just stop offering it.

- Reduce It: This involves putting controls in place to lower the risk's likelihood or its impact. To guard against cybersecurity threats, you might install better security software and train your team to spot phishing emails.

- Transfer It: Why shoulder the burden alone? This strategy shifts the financial fallout of a risk to a third party. The most common example is buying business insurance. A general liability policy transfers the financial risk of a lawsuit from your shoulders to the insurer's.

- Accept It: For some low-impact, low-likelihood risks, the most sensible approach is to do nothing and simply accept the potential consequences. This isn't ignoring the risk; it's making a conscious decision that the cost of fixing it outweighs the potential harm. You might accept the minor risk of a power outage by knowing you can just decamp to a coffee shop for a few hours.

Step 3: Monitor Your Controls

A risk management plan isn’t a "set it and forget it" kind of document. It's a living tool that needs regular attention. After you put your mitigation strategies in place, you have to check in to make sure they're actually working.

Are your new safety protocols being followed? Is your data backup system running correctly? Is your insurance coverage still adequate for your current operations? Monitoring means setting up checkpoints to track these things and ensure your defenses are holding strong.

Step 4: Review and Refine the Process

Finally, this whole framework is a cycle. Your business will change, new technologies will pop up, and market conditions will shift. As that happens, new risks will emerge and old ones might fade away. That’s why you need to formally review your entire risk management plan on a regular basis.

A quarterly check-in is a good rhythm for most small businesses, with a more in-depth review at least once a year. This is your chance to identify new threats, reassess existing ones, and tweak your strategies. For example, if you're managing a bunch of contracts, a regular review is critical to catch shifting obligations or liabilities. For more on that specific area, check out our guide on how to approach a small business risk management plan with a focus on legal agreements.

This continuous loop of assessing, mitigating, monitoring, and reviewing is what keeps your business resilient and ready for whatever comes next.

Your Action Plan for Digital and Cyber Threats

In a totally connected world, one of your biggest vulnerabilities is digital. Cybercriminals are actively hunting for small businesses, often banking on the fact that they're less prepared and defended than massive corporations. It's a huge risk management challenge that needs a clear, straightforward plan.

The numbers are pretty shocking. A whopping 43% of all cyberattacks specifically target small businesses. What's even more alarming is that only 14% have protective measures in place, creating a dangerous gap between the threat and their readiness. And the most common way criminals get in? Phishing. A full 57% of these attacks start with a sneaky email designed to steal credentials. You can dig into more small business statistics to see just how big this problem is.

This isn’t about scaring you; it’s about getting you ready. You don’t need a giant IT department to build a strong defense. Simply focusing on the basics of good cyber hygiene can dramatically lower your risk, and it's a critical piece of risk management for any small business.

Fortify Your First Line of Defense: Your Team

Your employees are your greatest asset, but they can also be your biggest vulnerability. A single click on a malicious link can blow past even the most expensive firewalls. That’s why consistent, hands-on training isn't just a nice-to-have—it’s non-negotiable.

Here are a few simple ways to turn your team into a human firewall:

- Conduct Phishing Simulations: Regularly send out fake phishing emails to your staff. These controlled tests are the perfect way to teach them how to spot red flags—like urgent demands, weird sender addresses, or generic greetings—in a safe setting.

- Establish Clear Reporting Protocols: Make sure every single person on your team knows exactly what to do when a suspicious email lands in their inbox. They should never click or reply. Instead, they need to report it immediately to a designated person or team.

- Hold Brief, Regular Training Sessions: Cyber threats are always changing. Short, monthly or quarterly security briefings are way more effective than one long, boring annual training. Keep it simple and focused on what’s happening right now.

The goal of training isn't to turn every employee into a cybersecurity guru. It's about building a culture of healthy skepticism, where pausing to question an unusual email becomes second nature. This simple habit is one of the most powerful defenses you can possibly build.

Implement Essential Technical Safeguards

While a sharp, vigilant team is your first line of defense, you need to back them up with some foundational technical controls. Think of these as powerful safety nets, ready to catch any threats that might slip through the cracks. They are surprisingly easy to set up and offer a massive return on investment when it comes to security.

Here are the absolute non-negotiables:

- Multi-Factor Authentication (MFA): This is arguably the single most effective security measure you can put in place. MFA requires a second form of verification (like a code sent to a phone) on top of a password. So even if a criminal manages to steal a password, they're stopped dead in their tracks without that second factor.

- Automated Data Backups: Just imagine losing all your customer data, financial records, and operational files overnight. A reliable backup system prevents this nightmare from becoming a reality. Use a service that automatically and regularly backs up all your critical data to a separate, secure location.

- Consistent Software Updates: Outdated software is riddled with known security holes that criminals absolutely love to exploit. Turn on automatic updates for all your computers, servers, and software to ensure these vulnerabilities get patched the moment fixes are released.

Uphold Basic Data Privacy Compliance

Beyond just stopping direct attacks, you have a responsibility to protect the customer and employee data you handle. A failure here can lead to a damaged reputation and some very expensive fines.

Start by getting a clear picture of what data you collect and why you need it. A good rule of thumb is to only gather what is absolutely essential for your business to run. Make sure any sensitive information is stored securely, with access limited only to those who truly need it.

Creating a simple data privacy policy that outlines how you handle information does two things: it builds trust with your customers and gives your team clear guidelines to follow. It's a proactive step that helps you head off compliance risks before they turn into legal headaches.

Protecting Your Money and Avoiding Legal Traps

While it's easy to get caught up in big-picture strategies, some of the biggest threats to your business are far more immediate. Think cash flow crunches and surprise lawsuits. These are the kinds of problems that can stop even the most promising business dead in its tracks.

That’s why protecting your finances and staying on the right side of the law are the cornerstones of practical risk management for small business. Think of your finances as your business's immune system and your legal setup as its shield. Without both, you're left exposed. Let's walk through how to reinforce them.

Fortifying Your Financial Foundation

A healthy bank account gives you something priceless: flexibility. It lets you survive the slow months and jump on unexpected opportunities. Building this financial resilience isn't about complex market predictions; it’s about a few core, disciplined habits.

First things first: build an emergency fund. This isn't your everyday operating cash. It's a separate, untouchable stash with 3-6 months of essential operating expenses. It's the safety net that lets you make payroll when a client pays late or cover an emergency equipment repair without taking on high-interest debt.

You also need to be proactive about getting paid. Set crystal-clear payment terms, send your invoices the moment a job is done, and have a system for following up on late payments. A predictable cash flow is your single best defense against financial instability.

A line of credit is something you should set up when you don't need it. Applying when your books are strong gives you the best chance of approval, and it provides a powerful backup resource you can tap into during a cash crunch. It keeps you from making panicked decisions later on.

Navigating the World of Legal Risks

Legal issues can feel overwhelming, but burying your head in the sand is never a good strategy. The good news? You don't need a law degree to protect your business. You just need to be proactive and insist on clear, written agreements for everything.

Every time you work with a client, hire an employee, or partner with a vendor, it should be backed by a solid contract. These aren’t just formalities. They are your best tools for setting expectations and defining what happens when things don't go as planned. A handshake deal is just a "he said, she said" argument waiting to happen.

Here are a few key areas that trip up many small businesses:

- Employment Laws: Get the basics right on hiring, classifying employees vs. contractors, and workplace safety. Simple mistakes here can lead to massive penalties.

- Intellectual Property (IP): Your brand name, logo, and unique products are valuable. Take the basic steps to protect your IP with trademarks or copyrights so no one else can cash in on your hard work.

- Data Privacy: If you collect any customer data—even just email addresses—you are legally on the hook to protect it. Cyberattacks are a huge threat, and a data breach can have devastating consequences.

Don’t underestimate the financial fallout of a single unmanaged risk. A stunning 46% of all cyber breaches hit companies with fewer than 1,000 employees. In 2021, 61% of SMBs were targeted by a cyberattack, with damages often running into the hundreds of thousands.

Demystifying Legal Documents with Modern Tools

One of the biggest hurdles for small business owners is dealing with legal documents. They’re expensive to have reviewed and often written in dense, confusing language. Paying a lawyer for every single contract just isn't realistic for most.

This is where technology can be a game-changer.

Tools like Legal Document Simplifier use AI to scan complex legal text and translate it into plain, understandable English. In seconds, you can see the key terms, critical deadlines, and potential red flags without having to be a legal expert yourself.

By highlighting what you’re on the hook for and where the potential dangers lie, these tools empower you to make smarter, faster decisions. It’s a perfect example of managing legal risk effectively and affordably. To get a better handle on these foundational topics, check out our guide on small business legal requirements.

Building Your First Risk Management Plan

Once you’ve identified and assessed the potential threats to your business, it’s time to pull it all together. The goal is to create a powerful but simple document: your risk management plan. Don't worry, this isn't about writing a hundred-page binder that just gathers dust. This is about action, not administration.

At the heart of this plan is a document often called a risk register. Think of it as a straightforward spreadsheet or table that acts as your strategic roadmap. It’s where you’ll list every risk you’ve found, estimate its potential damage, decide how you'll handle it, and assign someone to own it.

Creating Your Risk Register

Your risk register is the central hub for managing risk in your small business. It’s what makes sure nothing slips through the cracks and that everyone on your team knows exactly what to do to protect the company. A good register should be simple enough to understand at a single glance.

For every single risk, your register needs to answer four key questions:

- What is the risk? Get specific. "Supply chain issues" is too vague. Instead, write something like, "Our primary packaging supplier goes out of business."

- What is the impact and likelihood? This is where you use that High-Medium-Low scale you developed earlier to focus on what truly matters.

- What is our response plan? Write down your chosen strategy—whether you plan to Avoid, Reduce, Transfer, or Accept the risk.

- Who is responsible? Name a specific person to monitor the risk and kick the response plan into gear if needed. This step is absolutely critical for accountability.

A risk register transforms abstract worries into a concrete action plan. It's the difference between saying, "I hope our server doesn't crash," and "If the server crashes, Jane will activate our cloud backup, and we'll be operational within an hour."

A Living Document for a Growing Business

Here’s the most important thing to remember: your risk management plan is not a static file you create once and forget. It has to be a living document that grows and changes right alongside your business. As you launch new products, bring on new team members, or expand into new markets, new risks will inevitably pop up.

Set a schedule to review your risk register—maybe a quick check-in quarterly and a deeper dive once a year. This regular maintenance ensures your plan stays relevant and effective. For example, as your company signs more and more contracts, the legal risks tied to them will grow. It's essential to perform regular reviews to fully grasp your obligations and potential liabilities. To get a handle on this, you can learn more about performing a contract risk assessment in our detailed guide.

By keeping your plan current, you’re building a more resilient and successful company—one that’s ready to navigate uncertainty and turn potential threats into managed outcomes.

Of course, here is the rewritten section, crafted to sound like it was written by an experienced human expert.

Got Questions About Business Risk? We’ve Got Answers.

Even with the best-laid plans, questions about managing risk always pop up. It's completely normal. Let's walk through some of the most common ones I hear from small business owners to clear up any confusion with some quick, practical advice.

How Often Should I Actually Look at My Risk Plan?

Think of your risk plan like a GPS for your business—it’s only useful if it reflects the current road conditions. For most small businesses, a quarterly check-in is a great rhythm to get into. A full, deep-dive review should happen at least annually.

But don’t just stick to the calendar. Your plan needs immediate attention after any major business shift. This could be:

- Launching a new product or service.

- Expanding into a new market.

- A big operational change, like switching to a new key supplier or adopting new technology.

The best risk plans are living documents, not something you create once and file away.

Your risk plan should be dynamic. It’s meant to be revisited not just on a schedule, but in direct response to what’s actually happening in your business. That’s how it stays relevant and keeps you protected.

I’m a Solopreneur. Do I Really Need a Formal Plan?

Yes, absolutely. While your plan might not be a 50-page binder like a larger corporation’s, the risks you face are just as real. In many ways, the stakes are even higher because you are the business. If something goes wrong, there’s no one else to pick up the slack.

A simple, written-down plan forces you to think systematically about what could go wrong. Things like client dependency (what happens if that one big client leaves?), income fluctuations, or a simple hard drive failure can be devastating. A plan makes your one-person operation much more resilient and ready for whatever comes your way.

What’s the Biggest Risk Most Small Businesses Miss?

Everyone’s talking about cybersecurity these days, and for good reason. But one of the most dangerous and commonly overlooked risks is what we call ‘key person’ dependency. This is when your entire operation hinges on the knowledge and skills of one or two people—usually the owner.

Think about it: if that key person gets sick, leaves the company, or is just unavailable for a while, everything can grind to a halt. Their irreplaceable knowledge walks out the door with them.

You can fight this by documenting your most important processes, cross-training team members where you can, and using shared systems. The goal is to make sure critical information isn't locked away in one person's head.

Navigating the legal side of risk, from contracts to compliance, can feel like a minefield. Legal Document Simplifier uses AI to instantly translate dense legal jargon into plain English. It helps you spot risks, understand your obligations, and track critical deadlines—all without the hefty attorney fees. Learn more and try Legal Document Simplifier today.