If you've ever stared at an indemnity clause in a contract, you know it can feel like trying to decipher another language. Let's cut through the legalese. Simply put, indemnification is a contractual promise from one party to cover the financial losses of another if something goes wrong.

Think of it as a financial safety net woven directly into your agreement.

Breaking Down the Promise of Indemnification

Here’s a real-world scenario to make it click. Imagine you hire a freelance graphic designer to create a logo for your new company. Unfortunately, the designer uses a copyrighted image without getting the proper license, and the image owner decides to sue your business for infringement.

If your contract has a solid indemnification clause, the designer is on the hook. They've promised to pay for your legal defense and any damages you're ordered to pay. This is a classic risk-shifting tool; it pushes the financial consequences of an error back onto the person who made it. This isn't a new concept—it's been a bedrock of commercial agreements for ages, helping businesses clearly assign risk.

Who Is Involved in Indemnification

To really get what indemnification means, you have to know the players. Every clause has two main roles, and knowing who's who is the first step to understanding what you're signing.

- The Indemnitor: This is the one making the promise—the one who agrees to pay. In our example, the graphic designer is the indemnitor. They are shouldering the financial responsibility.

- The Indemnitee: This is the party being protected. Your business is the indemnitee because the clause shields you from the financial fallout.

When someone agrees to indemnify you, they're essentially acting as a private insurance policy for a specific set of risks defined in the contract.

Nailing down these roles is critical because the specific wording of the clause spells out the entire relationship and what each party is responsible for. The language can be dense, which is why taking the time for some legal jargon translation is a non-negotiable for any professional or small business owner. Once you break these ideas down, you can walk into any contract negotiation with much more confidence.

Anatomy of an Indemnification Clause

An indemnification clause isn't just a single sentence; it's a finely-tuned legal engine with several critical parts working together. To truly understand the protection you're getting (or giving up), you need to know how this engine is built. Think of it like a mechanic looking under the hood—each component has a very specific function.

When you first read one, you'll almost always see a powerful trio of verbs: indemnify, defend, and hold harmless. They might sound like legal fluff, but each one carries a distinct weight and responsibility.

- To Indemnify: This is the core promise. It's the commitment to pay the other party back for any financial losses they've suffered from a covered incident. Essentially, it’s about making them financially whole again after the fact.

- To Defend: This is a much more immediate and active duty. It means the party giving the indemnity must step in right away to handle the legal defense for a claim, covering lawyers' fees and court costs as they happen.

- To Hold Harmless: This is the broadest shield. The goal here is to ensure the protected party isn't held legally responsible at all for the specified risk. It’s about preventing liability from ever sticking to them in the first place.

The Devil Is in the Details: Scope and Triggers

Beyond those core duties, the real power of the clause comes down to its scope and its triggers.

The scope defines exactly which losses are covered. Are we talking just about court-ordered damages, or does it include legal fees, settlement costs, and other expenses? A tightly defined scope is always safer for the person giving the indemnity.

Triggers are the specific events that set the entire clause in motion. A trigger could be a lawsuit for intellectual property infringement, a claim of negligence, or a simple breach of contract. The wording here is absolutely crucial. A clause triggered by "any and all claims" is a world away from one that only kicks in after a "final, non-appealable judgment."

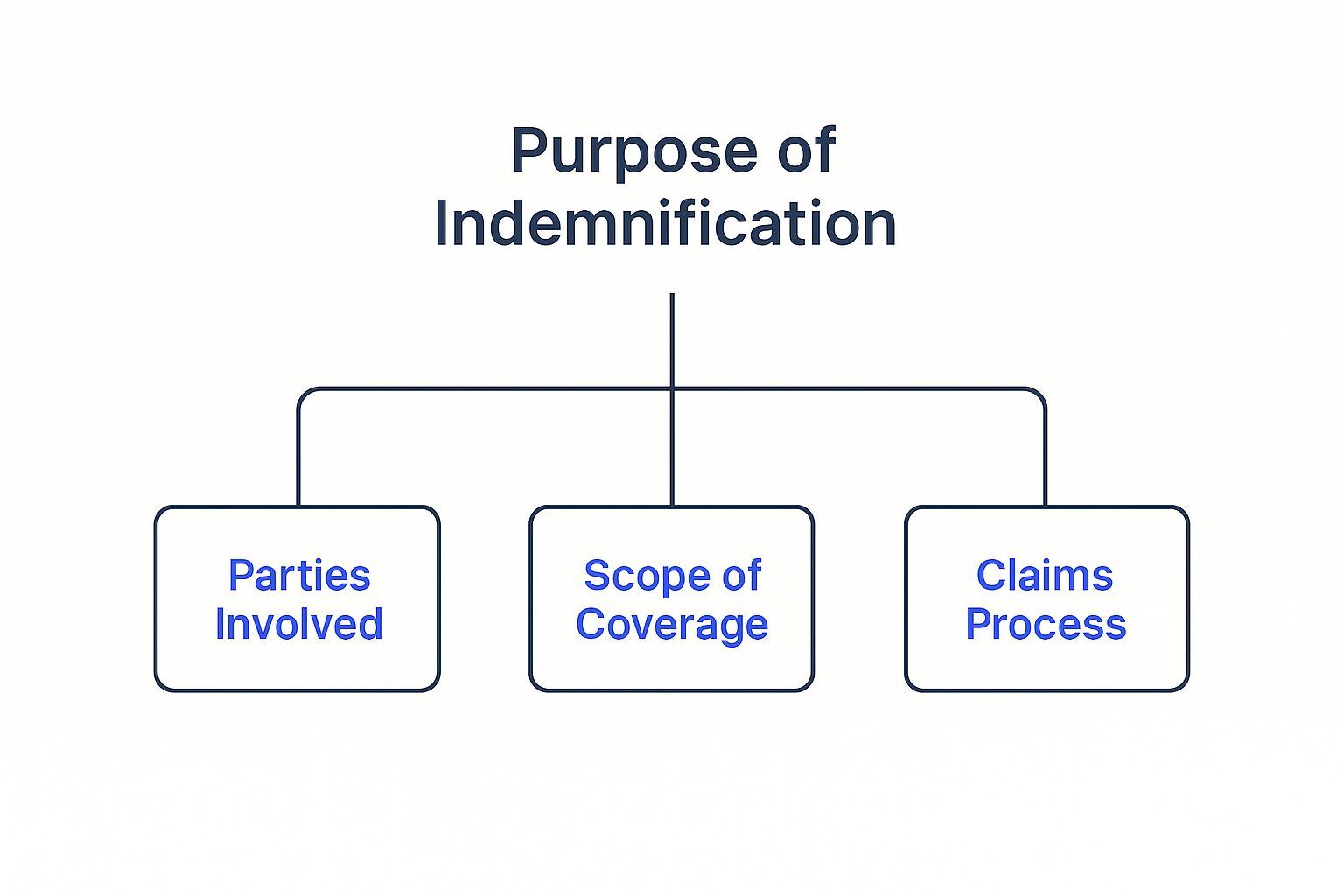

This image helps visualize how all these moving parts come together.

As the diagram shows, a solid indemnification clause clearly identifies the parties involved, specifies what's covered, and lays out a clear process for what happens when a claim arises.

To help you spot these components in your own contracts, let's break them down into a simple table. Each part of the clause has a specific job to do.

Key Elements of an Indemnification Clause

| Component | What It Means | Example Phrase |

|---|---|---|

| The Parties | Clearly identifies who is giving the indemnity (Indemnitor) and who is receiving it (Indemnitee). | "Consultant (the Indemnitor) agrees to indemnify the Client (the Indemnitee)..." |

| The Core Duties | Specifies the level of protection, often using the "indemnify, defend, and hold harmless" trio. | "...agrees to indemnify, defend, and hold harmless..." |

| The Scope | Defines the types of losses and damages that are covered under the agreement. | "...from and against any and all claims, losses, expenses, and damages (including reasonable attorney's fees)..." |

| The Trigger | Outlines the specific event or action that activates the indemnification obligation. | "...arising out of or resulting from the Consultant's negligent performance of the Services." |

Seeing these elements laid out makes it much easier to dissect a clause and understand its real-world impact.

Putting It All Together: A Real-World Example

Let's see how these pieces work together in a typical contract sentence:

"Consultant agrees to indemnify, defend, and hold harmless Client from and against any and all claims, losses, and expenses (including reasonable attorney's fees) arising out of or resulting from the Consultant's negligent performance of the Services."

In this example, the consultant provides all three layers of protection. The scope—"claims, losses, and expenses"—is fairly standard. But the most important part is the trigger: "Consultant's negligent performance." This means the consultant is only on the hook if they were actually careless.

Now, imagine you remove the word "negligent." The clause would now make the consultant responsible for issues even if they did their job perfectly. It’s a stark reminder of how a single word can completely shift the balance of risk in a contract.

The Three Main Types of Indemnity Clauses

When you see an indemnification clause in a contract, it's not a one-size-fits-all situation. These promises come in different flavors, each shifting risk in a very specific way. Think of them as different levels of financial responsibility—some are fair and balanced, while others can be incredibly lopsided.

There are three main types you’ll run into, and the difference between them is massive. Knowing how to spot them can be the difference between a fair deal and accepting a catastrophic amount of liability without even realizing it.

Let's ground this in a real-world scenario. A general contractor hires a subcontractor to install new windows on a building. While working, the subcontractor accidentally drops a window, injuring a pedestrian below. Who's on the hook for the inevitable lawsuit? The answer lies entirely in which type of indemnity clause they signed.

1. Limited Form Indemnity

This is the fairest of the bunch, often called a "comparative fault" clause. It’s pretty straightforward: you are only responsible for your own mistakes. Nothing more.

In our window-dropping scenario, if the subcontractor was 100% at fault, they'd indemnify the general contractor for all the legal costs and damages. But what if the general contractor contributed to the accident, maybe by failing to rope off the work area properly? Under a limited form clause, the subcontractor would only have to pay for their share of the fault. It’s the most equitable approach because liability is tied directly to who was actually negligent.

2. Intermediate Form Indemnity

Here’s where things start to get dicey for the one providing the indemnity. An intermediate form clause dramatically raises the stakes. With this clause, the subcontractor (the indemnitor) agrees to cover losses from their own negligence and, crucially, any losses that arise from shared or joint negligence.

Back to our construction site: if a court found both the subcontractor and the general contractor were partially to blame, the subcontractor would still have to cover all the damages. The only way the subcontractor gets out of paying is if the general contractor is found to be 100% solely negligent. It's a significant shift of risk, which is why many states have passed laws to restrict or regulate these types of clauses.

An intermediate form clause essentially says, "I'll take the blame for my mistakes and for our shared mistakes, but not for your mistakes alone."

You'll see this type often in construction and other high-risk fields, but it demands a very careful review before you sign.

3. Broad Form Indemnity

This is the most extreme and dangerous type of indemnity for the person agreeing to it. A broad form clause makes the subcontractor responsible for any and all losses related to the project—even if the general contractor was solely and completely at fault.

It’s almost hard to believe. Let's say the general contractor carelessly bumped the subcontractor’s ladder, causing the window to fall. With a broad form clause, the subcontractor would still be contractually forced to pay for the general contractor’s legal fees, settlements, and damages.

This arrangement is so lopsided that it’s banned or heavily restricted in most states. Forcing one party to pay for another party's sole negligence is generally seen as against public policy. If you ever see contract language that even hints at this level of risk transfer, huge red flags should go up immediately.

How Indemnification Protects High-Stakes Deals

Indemnification clauses aren't just for small-time service agreements. In the world of high-stakes business deals—think mergers and acquisitions (M&A)—they are an absolute cornerstone. This promise to cover losses is what gives a buyer the confidence to sign on the dotted line, protecting them from nasty surprises that might crawl out of the woodwork long after the deal is done.

Imagine you're buying a company. You’ve done your homework, combed through the financials, and everything looks clean. But what if there’s a massive, undisclosed tax liability from three years ago? Or a simmering lawsuit the seller conveniently forgot to mention? Without an indemnification clause, you, the new owner, are on the hook for those expensive problems.

This is exactly why thorough due diligence is so critical. A buyer has to sniff out potential risks before closing the deal to make sure the indemnification clause is drafted to cover them. To really get into the weeds of this process, check out our guide on business acquisition due diligence.

A Financial Safety Net for Buyers

In any M&A deal, the seller makes a series of promises about the business's health. These are called "representations and warranties." If it turns out one of those promises was false, the indemnification clause is the tool that makes the buyer financially whole again.

It's designed to shield the buyer from a whole host of potential nightmares:

- Undisclosed Lawsuits: A former employee sues for wrongful termination for something that happened years before the sale.

- Tax Liabilities: The IRS comes knocking, claiming the company owes back taxes.

- Intellectual Property Claims: A competitor emerges, claiming the company's flagship product infringes on their patent.

Let’s be honest, without this contractual backstop, the financial risks would be so massive that most acquisitions would simply fall apart. Indemnification is the glue that holds these complex, high-value deals together.

In an M&A deal, the indemnification clause is basically the seller saying: "If any skeletons fall out of the closet after you buy my company, I'll pay to clean up the mess."

The Rise of W&I Insurance

The sheer importance of indemnification has even given birth to a specialized financial product: Warranty & Indemnity (W&I) insurance. Instead of just hoping the seller has deep enough pockets to cover a claim, the risk can be transferred to an insurance company. The insurer steps in to cover losses from a breach of warranty, which helps smooth things over for everyone involved.

This clever solution has become a huge part of modern deal-making. In fact, the global W&I insurance market was valued at USD 3.2 billion and is expected to more than double to USD 7.2 billion by 2032. You can find more details on the growth of the Warranty and Indemnity services market on verifiedmarketresearch.com. This explosive growth tells you everything you need to know about how vital this protection has become.

By turning a contractual promise into an insurable risk, W&I insurance helps get deals over the finish line. It bridges gaps in negotiations and gives buyers an extra layer of security, ultimately fueling business transactions across the globe.

Indemnity for Consultants and Service Professionals

If you’re a consultant, designer, or developer, you’ve seen it: the indemnification clause. It's not just another chunk of legal jargon; it’s a direct measure of your professional liability. When you’re hired for your expertise, clients will almost always require this clause to ensure you stand behind your work.

Put yourself in their shoes. They're paying you for a specific skill. If that work backfires and leads to a lawsuit—maybe a web developer’s code has a security hole that causes a data breach—the client wants a guarantee that they won't be stuck with the legal bills. This is what indemnification does in a service agreement: you promise to cover the client's losses if your work creates a specific kind of problem.

The Role of Professional Indemnity Insurance

This contractual promise has a critical real-world partner: Professional Indemnity Insurance (PII). You might also hear it called Errors & Omissions (E&O) insurance. This coverage is specifically designed to back up the indemnification promises you make in your contracts. When you agree to protect a client from claims of negligence or error, your PII policy is what pays for the lawyers and any potential settlements.

Without it, a single lawsuit could wipe you out financially. PII is the financial backbone that makes your professional promises possible, and it’s a non-negotiable cost of doing business safely. It’s no surprise the global market for this insurance is massive, valued at around USD 37.2 billion, and growing. You can see more data on the professional indemnity insurance market on custommarketinsights.com.

For a consultant, an indemnification clause without PII is like writing a check you don't have the funds to cover. The insurance is what makes your promise credible.

Navigating Client and Regional Expectations

The need for this protection is also driven by what clients and local laws demand. Big corporate clients, for example, often require their independent contractors to carry a certain minimum level of PII. For professionals working abroad, understanding the terms in your UAE employment contract is crucial, as regional regulations can heavily influence your liability.

These clauses rarely exist in a vacuum. They often tie into other contractual standards that define the scope and risks of your duties. If you’re interested, you can learn more about this in our guide on what is a service level agreement.

At the end of the day, having solid PII and carefully negotiating your indemnity clauses are fundamental to building a resilient and sustainable professional practice.

What to Check Before You Sign an Indemnity Clause

Before your pen ever touches paper, taking a hard look at the indemnification clause is one of the most important things you can do to protect your business. You don't need a law degree to spot the red flags; you just need to know what you're looking for.

This isn't about finding loopholes. It's about approaching the contract with a clear strategy to identify unfair terms and negotiate an agreement that feels more like a partnership and less like a liability trap.

Examine the Scope and Triggers

First, get a feel for the scope. Is it too broad? A clause that makes you responsible for "any and all claims" is a massive red flag. You want to see specific, narrow language that clearly defines which losses are covered and connects them directly to something you did or failed to do.

Next, figure out what the triggers are. In other words, what specific event makes you financially responsible? A fair trigger is something concrete, like a final court judgment. A lopsided one could be the mere filing of a claim, which could stick you with legal bills before anyone has even decided who's at fault.

Look for Caps and Mutuality

Even with a fair scope, the potential financial hit could be massive. This is where a liability cap becomes your best friend. A cap limits your total obligation to a specific dollar amount—maybe the total value of the contract or the limit of your insurance coverage. Without one, you're looking at potentially unlimited liability.

Finally, ask yourself if the clause is a one-way street. Mutuality is all about fairness. If you're being asked to indemnify the other party, it's perfectly reasonable to ask for the same protection in return. They should be responsible for their mistakes, just as you are for yours.

A one-sided indemnity clause isn't a partnership; it's a transfer of almost all the risk onto your shoulders. Always push for a fair, two-way agreement where each party is responsible for their own actions.

When expanding your business, it’s also wise to understand the local landscape, including the legal requirements for starting a business in Turkey if you're operating there. Paying close attention to these four key areas—scope, triggers, caps, and mutuality—will help you sign agreements that protect your interests instead of putting them at risk.

Your Top Indemnification Questions, Answered

Once you start wrapping your head around indemnification, you’ll naturally have more specific questions. Getting clear on these details is what really cements your understanding and shows you how these clauses play out in the real world. Let's dig into a few of the most common ones.

Is Indemnification Just Another Word for Insurance?

It's easy to see why people mix these two up. Both are about protecting you from financial loss, but they get there in completely different ways.

Think of it like this: indemnification is a direct promise between two parties in a contract. Party A promises to cover Party B if a specific problem arises. It's a one-to-one agreement.

Insurance, on the other hand, involves bringing in a third party—the insurance company. You pay them a premium, and they agree to cover you for certain risks outlined in a policy. A savvy business will often use its insurance policy as the financial backstop to fulfill an indemnification promise it made in a contract.

Are Indemnity Clauses Always Enforceable?

Absolutely not. You can’t just write whatever you want into a contract and expect a court to back it up. A judge can—and often will—toss out an indemnity clause if it’s wildly unfair, too vague, or goes against public policy.

For instance, clauses that try to force someone to pay for another party's intentional wrongdoing or gross negligence rarely hold up in court.

The big takeaway here is that enforceability is never a guarantee. Contract law can change dramatically from one state or country to the next, so an overly aggressive clause that works in one place might be totally useless somewhere else.

This is where a little legal guidance can save you a lot of future headaches.

What’s the Big Deal About the "Duty to Defend"?

The “duty to defend” is a crucial component that can be added to an indemnification clause, and it’s a game-changer. It means the indemnifying party doesn't just have to pay the final bill for damages—they have to step in and pay for the lawyers and legal fees from the very beginning.

Imagine getting sued. Without a duty to defend, you’d be paying your legal bills out of pocket for months, maybe even years, hoping to get reimbursed later. With it, the other party is on the hook for those costs right away. It's an immediate shield against the crushing cost of litigation, offering a much stronger layer of protection than just waiting for a final judgment.

Feeling like you need a law degree to understand your own contracts? Legal Document Simplifier uses AI to translate dense legal jargon into plain English. Upload your document and get a clear, actionable summary in minutes so you know exactly what you’re signing. Get your clear summary now at legaldocumentsimplifier.com.